Economic Survey 2025-26

Content

- Introduction

- State of the Indian Economy

- Fiscal Developments

- Monetary Management

- External Sector

- Agriculture

- Services Sector

- Key Challenges

Introduction

The Union Minister for Finance and Corporate Affairs tabled the Economic Survey 2025–26 in Parliament ahead of the Union Budget. The Survey presents India as a stable, resilient, and investment-ready economy, navigating global uncertainty while strengthening its domestic economic foundations.

The Survey is an annual document prepared by the Economic Division of the Ministry of Finance under the Chief Economic Adviser (CEA). It evaluates macroeconomic performance, sectoral trends, structural challenges, and future prospects. First introduced in 1950-51 as part of the Budget, it has been presented as a separate document since 1964.

State of the Indian Economy: Growth with Stability

The Survey notes that while global growth remains resilient, risks persist due to geopolitical tensions, trade fragmentation, and financial market stress.

- As per the First Advance Estimates, India’s Real GDP growth for FY26 is placed at 7.4%, with GVA growth at 7.3%.

- Looking ahead, India is expected to grow at 6.8-7.2% in FY27, reaffirming its position as the fastest-growing major economy for the fourth consecutive year.

- On the demand side, Private Final Consumption Expenditure (PFCE) grew by 7.0% in FY26, reaching 61.5% of GDP, the highest since 2012. This was supported by:

- Low inflation and stable employment conditions

- Rising real incomes

- Strong rural demand driven by agriculture

- Revival in urban consumption aided by tax rationalisation

- Investment activity strengthened, with Gross Fixed Capital Formation (GFCF) growing by 7.8%, sustaining a healthy 30% share of GDP, driven mainly by public capital expenditure and a revival in private investment.

- On the supply side, services remained the primary growth engine, with services GVA estimated to grow at 9.1% during the year.

Fiscal Developments

The Survey highlights that prudent fiscal management has enhanced India’s macroeconomic credibility.

- Centre’s revenue receipts increased from about 8.5% of GDP (FY16–20) to 9.2% in FY25 (PA), largely due to higher non-corporate tax collections.

- The direct tax base expanded significantly, with income tax return filers increasing from 6.9 crore (FY22) to 9.2 crore (FY25).

- GST collections during April–December 2025 stood at ₹17.4 lakh crore, registering 6.7% year-on-year growth.

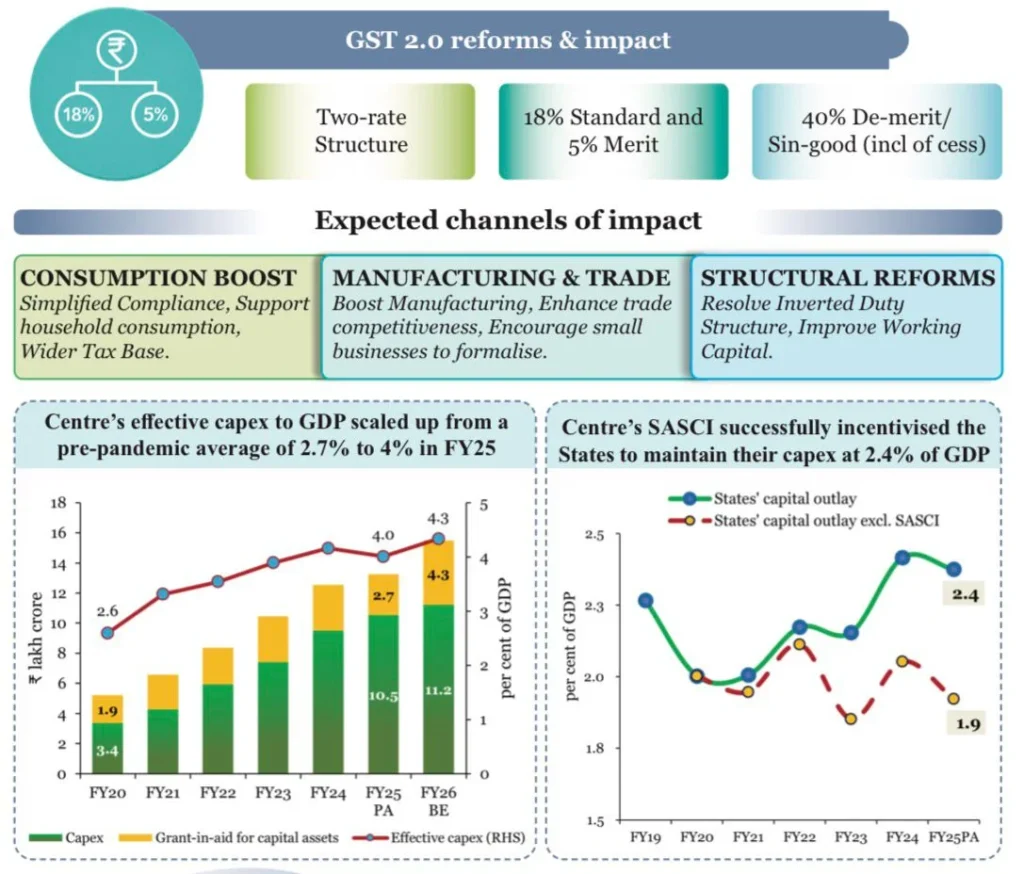

- The Survey proposes GST 2.0, with a simplified two-rate structure aimed at boosting consumption, improving compliance, and enhancing manufacturing competitiveness.

- Centre’s effective capital expenditure rose from a pre-pandemic average of 2.7% of GDP to nearly 4% in FY25, while Special Assistance to States for Capital Expenditure (SASCI) incentivised states to maintain high capital outlays.

- Even as state fiscal deficits rose slightly to 3.2% of GDP in FY25, India managed to reduce its general government debt-to-GDP ratio by about 7.1 percentage points since 2020.

Monetary Management and Financial Intermediation

India’s monetary and financial system performed robustly during FY26 (April-December 2025).

- The banking sector’s asset quality improved sharply, with Gross NPAs at 2.2% and Net NPAs at 0.5% (September 2025).

- Credit growth accelerated to 14.5% YoY by December 2025, supporting investment and consumption.

- Financial inclusion deepened through:

- PM Jan Dhan Yojana, with 55.02 crore accounts

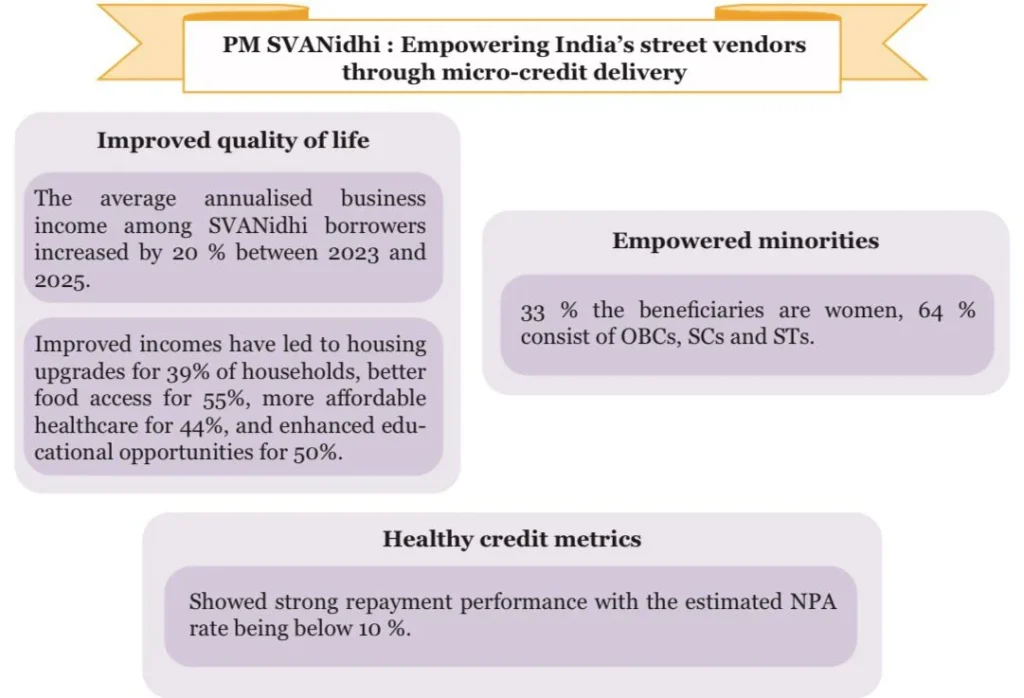

- Credit expansion via PMMY, Stand-Up India, and PM SVANidhi

- PMMY alone disbursed ₹36.18 lakh crore across 55.45 crore loan accounts

- Capital market participation surged, with:

- Over 21.6 crore demat accounts

- Nearly 12 crore unique investors, about 25% women

- The IMF-World Bank Financial Sector Assessment Program (FSAP) 2025 validated India’s resilient and well-capitalised financial system, noting adequate buffers even under severe stress scenarios.

External Sector: Expanding Global Footprint

India’s external sector showed marked strengthening.

- India’s share in global merchandise exports rose from 1% to 1.8%, and services exports from 2% to 4.3% between 2005 and 2024.

- UNCTAD’s Trade and Development Report 2025 ranked India third in the Global South in trade partner diversification.

- Total exports reached a record USD 825.3 billion in FY25, driven by an all-time high services exports of USD 387.6 billion.

- The current account deficit remained moderate at ~1.3% of GDP, supported by strong services exports and record remittances of USD 135.4 billion.

- Forex reserves rose to USD 701.4 billion, providing an import cover of nearly 11 months.

- Despite global headwinds, India attracted USD 64.7 billion in FDI (Apr–Nov 2025) and ranked 4th globally in Greenfield investments.

Inflation: Historic Moderation

India recorded its lowest-ever CPI inflation, with average headline inflation at 1.7% during Apr-Dec 2025.

- The decline was driven largely by disinflation in food and fuel, which together account for over half of the CPI basket.

Among major EMDEs, India witnessed one of the sharpest inflation declines, supporting consumption and macroeconomic stability.

Agriculture and Food Management

The agriculture sector displayed strong performance.

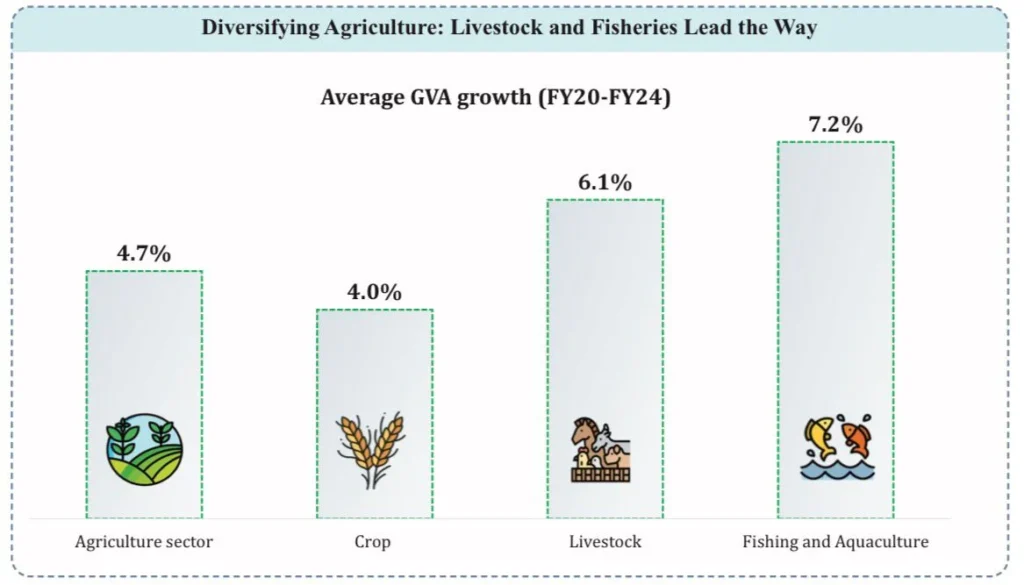

- Livestock GVA rose by nearly 195% between FY15 and FY24, while fish production increased by over 140%.

- Supported by a good monsoon, foodgrain output reached a record 3,577.3 LMT in AY 2024–25.

- Horticulture, accounting for about 33% of agricultural GVA, emerged as a key growth driver.

- Schemes such as PM-KISAN, AIF, e-NAM, MSP, and PM-KMY strengthened farm incomes and resilience.

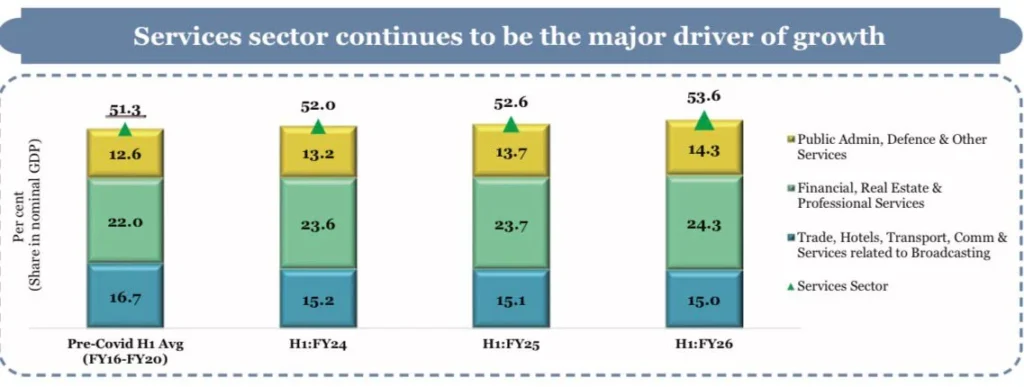

Services Sector: Engine of Growth and Employment

- India is the 7th-largest services exporter, with services accounting for ~80% of total FDI inflows in FY23–FY25.

The services sector has become India’s primary interface with the global economy, driving foreign exchange earnings and investor confidence. Strong performance in IT services, business process management, financial services, tourism, and professional services has attracted sustained foreign investment, making services the largest recipient of FDI in recent years. - The sector provides 30% of total employment and nearly 62% of urban employment.

Services form the backbone of India’s labour market, particularly in urban areas, absorbing a large share of skilled and semi-skilled workers. The sector plays a crucial role in job creation, income generation, and supporting India’s expanding middle class, while also acting as a stabiliser during periods of industrial or agricultural slowdown.

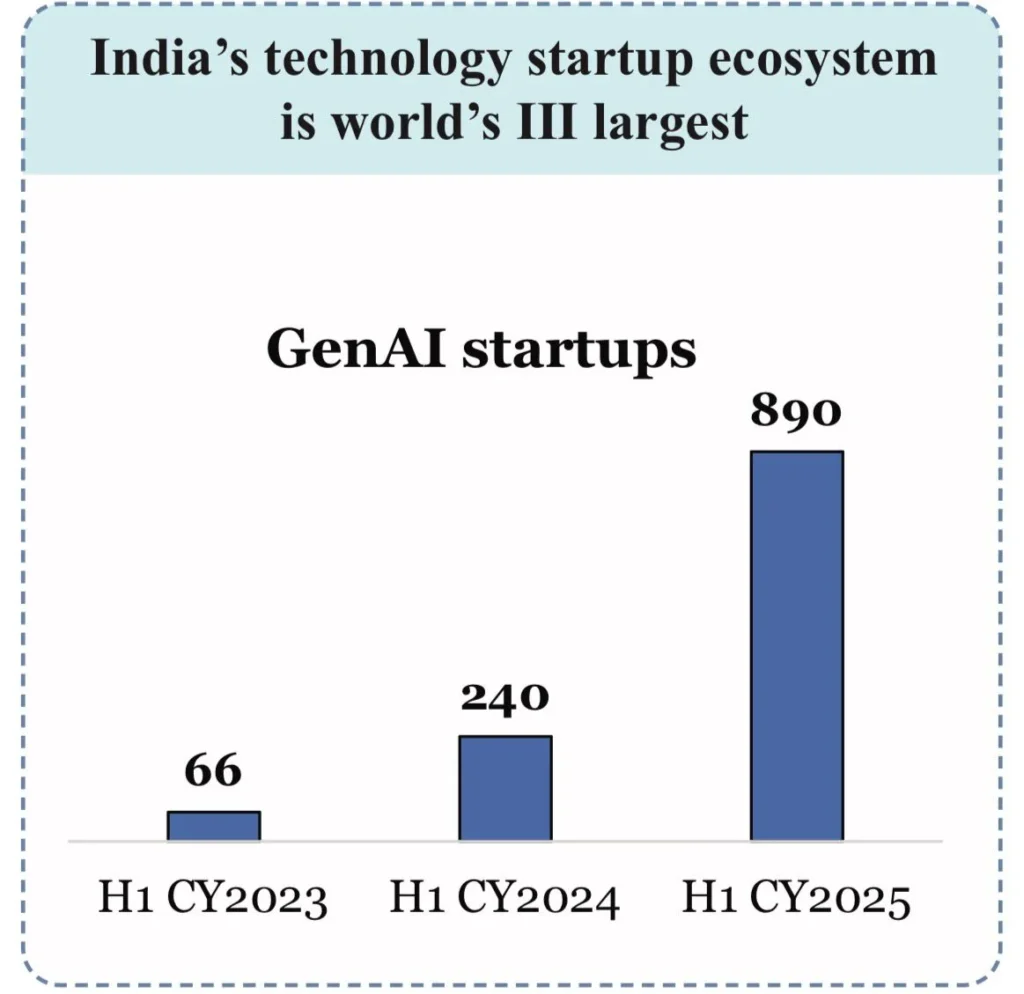

- India has emerged as a global hub for Global Capability Centres (GCCs) and technology startups, including rapid growth in GenAI ventures.

Multinational companies increasingly locate their GCCs in India to leverage cost efficiency, a skilled workforce, and a strong digital ecosystem. Alongside this, India’s startup ecosystem especially in artificial intelligence and generative AI, is scaling rapidly, positioning the country as a key player in advanced digital services and innovation-led growth.

Key Challenges Highlighted

1. Rising Geopolitical Fragmentation and Supply-Chain Weaponisation

- The global economy is moving away from rules-based globalisation towards geopolitical blocs and strategic trade controls.

- Sanctions, export restrictions, and technology embargoes have increased uncertainty in access to energy, critical minerals, and advanced technologies, raising India’s exposure to external shocks.

- This fragmentation complicates India’s deeper integration into global value chains and increases vulnerability to global disruptions.

2. Weak State Capacity and Bureaucratic Risk Aversion

- The Survey identifies weak state capacity as the key internal constraint on India’s growth.

- Fear of audits, vigilance action, and retrospective scrutiny has encouraged risk-averse decision-making, slowing policy execution.

- Temporary policies often persist due to policy inertia, reducing flexibility and limiting mission-oriented governance.

3. Expansion of Unconditional Cash Transfers

- While cash transfers provide short-term relief, their rapid expansion raises concerns over fiscal sustainability.

- Rising revenue expenditure risks crowding out capital expenditure, especially in States with revenue deficits.

- Over-reliance on transfers may weaken incentives for productivity-enhancing investments and long-term growth.

4. High Logistics and Energy Costs

- Elevated logistics and energy costs act as an implicit tax on manufacturing, reducing competitiveness.

- Despite infrastructure improvements, inefficiencies in transport and supply chains keep logistics costs high.

- High input costs weaken India’s export competitiveness and constrain scale expansion in manufacturing.

5. Underinvestment in R&D and Frontier Manufacturing

- The Survey flags low private sector investment in R&D, limiting innovation capacity.

- India lags in frontier manufacturing due to weak linkages between industry, research, and technology development.

- This constrains India’s ability to move up the value chain and sustain long-term industrial competitiveness.

Conclusion

The Economic Survey 2025-26 presents India not merely as a resilient economy, but as a rising anchor in the global economic order. While macroeconomic fundamentals remain strong, achieving Viksit Bharat will depend on bridging the gap between policy ambition and execution, building state capacity, and embedding India deeply into global value chains.