Mutual Credit Guarantee Scheme (MCGS)

Content

- Why in News?

- Introduction

- Key Features of the Scheme

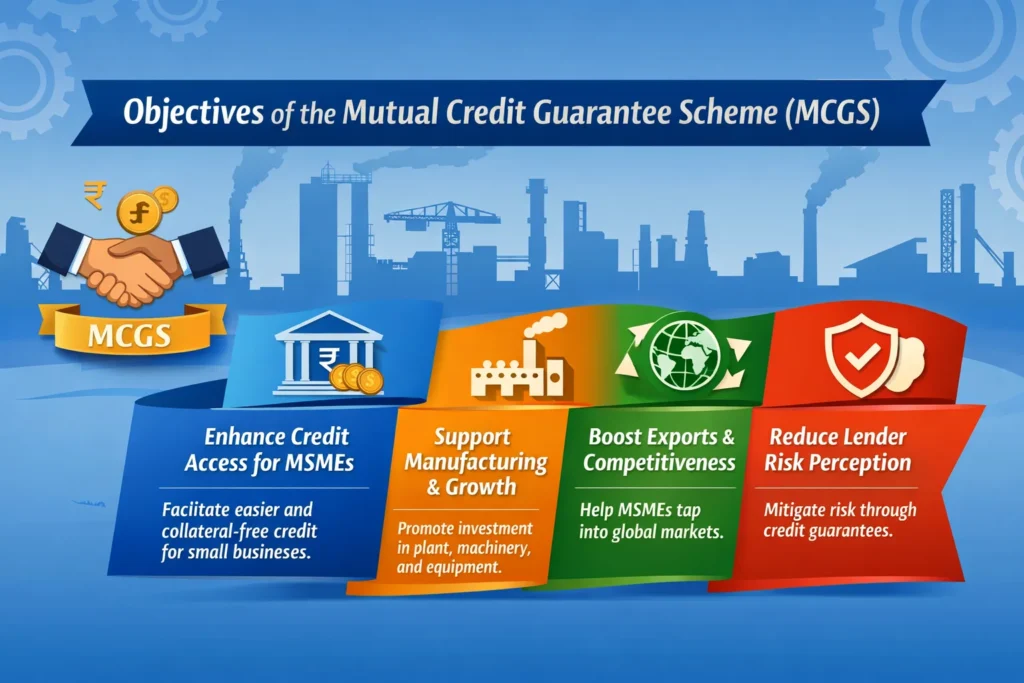

- Objectives

- Significance

- Key Modifications

- Challenges

- Conclusion

Why in News?

The Government of India has recently revised the Mutual Credit Guarantee Scheme (MCGS) to expand credit access for MSMEs, with a specific focus on investment in plant and machinery and boosting manufacturing and exports.

Introduction

The Mutual Credit Guarantee Scheme (MCGS) is a government-backed initiative aimed at improving access to institutional credit for Micro, Small and Medium Enterprises (MSMEs). One of the major constraints faced by MSMEs in India is the lack of collateral, which limits their ability to secure loans from formal financial institutions.

To address this issue, the scheme provides a partial credit guarantee to lenders, thereby reducing the risk associated with lending to MSMEs. This encourages banks and financial institutions to extend loans for productive investments, particularly in the manufacturing sector. The scheme is implemented through the National Credit Guarantee Trustee Company Limited (NCGTC) under the Ministry of Finance.

Key Features of the Scheme

The scheme provides a credit guarantee cover of up to 60% on loans extended by member lending institutions to eligible MSMEs. This partial guarantee mechanism reduces the exposure of lenders and incentivises them to finance relatively riskier but productive enterprises.

- It primarily covers term loans of up to ₹100 crore, which are intended for the purchase of plant, machinery, and equipment. By focusing on capital expenditure rather than working capital, the scheme aims to promote long-term industrial growth and capacity expansion.

- Eligibility under the scheme requires MSMEs to have valid Udyam Registration, which also contributes to the formalisation of enterprises. Another important condition is that a significant proportion of the loan amount must be utilised for investment in machinery and equipment, ensuring that credit is directed towards productive use.

- The scheme is operational for a fixed duration or until a specified guarantee limit is reached, reflecting a targeted and time-bound approach to credit support.

Objectives

- The primary objective of MCGS is to enhance the flow of credit to MSMEs, particularly those that face challenges in accessing finance due to lack of collateral or credit history.

- It also aims to support the growth of the manufacturing sector by enabling firms to invest in modern machinery and technology.

- In doing so, the scheme aligns with broader national initiatives such as Make in India and the push for export-led growth.

- Additionally, the scheme seeks to reduce the risk perception among lenders, thereby strengthening the overall credit ecosystem for small businesses.

Significance

- The significance of MCGS lies in its potential to address one of the most critical bottlenecks in the MSME sector access to timely and adequate finance. By facilitating credit for capital investment, the scheme enables MSMEs to expand production capacity, adopt new technologies, and improve competitiveness.

- It also contributes to employment generation, as MSMEs are labour-intensive and play a key role in absorbing the workforce. Furthermore, by promoting formalisation through mandatory registration requirements, the scheme strengthens the integration of MSMEs into the formal economy.

- In the context of global trade, improved access to finance can help MSMEs enhance their export potential, thereby contributing to India’s external sector performance.

Key Modifications in Existing Scheme

| Parameter | Revised Provision |

| Upfront Contribution | 5% made refundable; 1% each refunded from 4th year onwards, subject to satisfactory loan performance |

| Eligibility | Extended to include Service Sector MSMEs |

| Machinery/Equipment Cost Requirement | Reduced to 60% of project cost (earlier 75%) |

| Guarantee Tenure | Fixed at 10 years |

Special Provisions for Exporter MSMEs

| Parameter | Provision |

| Eligible Exporters | Profitable MSMEs exporting at least 25% of turnover in each of last 3 financial years + meeting export realisation conditions |

| Guaranteed Loan Amount | Up to ₹20 crore |

| Upfront Contribution | 2% of loan amount (max ₹40 lakh); 1% refundable in 4th & 5th year |

| Guarantee Coverage | 75% of amount in default |

| Guarantee Fee | Nil in first year; thereafter 0.50% annually on outstanding loan |

Challenges and Concerns

Despite its potential, the scheme faces certain challenges.

- Awareness among MSMEs about such schemes remains limited, which can restrict its reach.

- Procedural complexities and compliance requirements may also discourage smaller enterprises from availing benefits.

- There is also a risk of moral hazard and rising NPAs, as partial guarantees may lead to relaxed lending standards.

Therefore, effective monitoring and prudent lending practices are essential for the success of the scheme.

Conclusion

The Mutual Credit Guarantee Scheme represents a significant step towards strengthening the MSME sector by addressing credit constraints and promoting productive investment. Its focus on capital formation, combined with risk-sharing mechanisms, makes it a key policy tool for driving industrial growth, employment generation, and export expansion.