Capital Gains Tax (CGT)

Content

- Why in News?

- Introduction

- Capital Gains Tax?

- Classification

- Why Did the Government Remove

- Conclusion

Why in News?

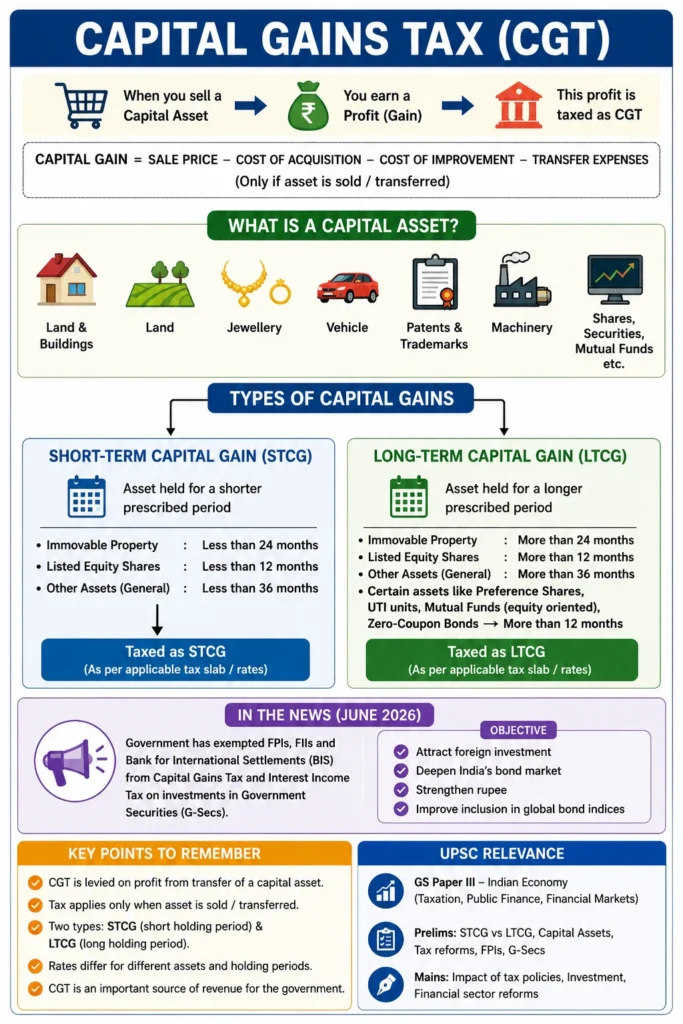

Capital Gains Tax has recently been in the news after the Government of India issued the Income-tax (Amendment) Ordinance, 2026, exempting Foreign Portfolio Investors (FPIs), Foreign Institutional Investors (FIIs), and the Bank for International Settlements (BIS) from paying tax on interest income and capital gains arising from investments in Government Securities (G-Secs). The move aims to attract foreign capital inflows, strengthen the rupee, deepen India’s bond market, and improve prospects for inclusion in major global bond indices.

Introduction

Capital Gains Tax (CGT) is one of the most important components of India’s direct tax system. It is levied on profits earned from the transfer or sale of a capital asset. Since such profits are treated as income under the Income Tax Act, they become taxable in the hands of the taxpayer.

Capital Gains Tax plays a significant role in revenue generation, wealth taxation, and regulation of investment behaviour. It affects individuals, businesses, investors, financial markets, and foreign investors alike.

For UPSC aspirants, the topic is important from the perspectives of taxation, public finance, economic reforms, financial markets, and investment policies.

What is Capital Gains Tax?

Capital Gains Tax refers to the tax imposed on the profit earned from the sale, transfer, exchange, or relinquishment of a capital asset.

The tax is applicable only when the asset is transferred and the gain is realized. Mere appreciation in the value of an asset does not attract capital gains tax unless the asset is sold or transferred.

The amount of capital gain is generally calculated as:

Capital Gain = Sale Price – Cost of Acquisition – Cost of Improvement – Transfer Expenses

Classification of Capital Gains

Capital gains are classified into two categories based on the holding period of the asset.

Short-Term Capital Gains (STCG)

Short-Term Capital Gain arises when a capital asset is sold within a specified period after acquisition.

For most assets, the holding period is less than 36 months.

For immovable property such as land and buildings, the period is less than 24 months.

For listed shares, equity-oriented mutual funds, and certain securities, a shorter holding period is prescribed under tax laws.

Since the asset is held for a relatively short duration, the resulting profit is treated as Short-Term Capital Gain and taxed accordingly.

Long-Term Capital Gains (LTCG)

Long-Term Capital Gain arises when an asset is held for a period exceeding the prescribed threshold.

For most assets, the holding period exceeds 36 months.

For immovable property, the holding period exceeds 24 months.

For listed equities, equity-oriented mutual funds, preference shares, securities, UTI units, and zero-coupon bonds, the holding period generally exceeds 12 months.

Long-term investments are generally encouraged through comparatively favourable tax treatment.

Why Did the Government Remove Capital Gains Tax on FPIs?

The decision was driven by several economic considerations.

India has experienced foreign portfolio outflows, rising global uncertainty, and pressure on the rupee. Attracting foreign investment into government bonds can help strengthen external sector stability.

The government also seeks to deepen India’s bond market and improve the attractiveness of Indian government securities relative to competing emerging markets.

Another objective is to enhance India’s prospects of inclusion in major global bond indices, which could bring long-term and stable capital inflows into the economy.

Conclusion

Capital Gains Tax is a crucial component of India’s taxation framework and plays an important role in shaping investment behaviour, financial market development, and government revenue generation. The recent exemption granted to FPIs on investments in Government Securities reflects India’s broader strategy of attracting foreign capital, strengthening the bond market, and improving external sector stability. As India continues its journey toward becoming a major global economic power, reforms in capital gains taxation will remain a key policy tool for balancing growth, investment, and fiscal sustainability.

Visit LevelUp IAS- Click Here